Roth IRA

By Brian McGeough, CFP® & Relationship Manager

A Roth conversion can be one of the most impactful tax planning moves available - but timing and execution matter. This note explains how it works and what to consider before acting.

What Is a Roth IRA?

A Roth IRA is an individual retirement account funded with after-tax dollars. Once inside the account, all capital gains and income grow tax-free — and qualified withdrawals in retirement are never taxed. There are also no required minimum distributions (RMDs) during the owner's lifetime. It is one of the most powerful long-term savings tools available, especially for young people with many working years ahead of them.

Why a Roth IRA Is Especially Powerful for Young People

A Roth IRA is one of the most powerful investment vehicles available — particularly for young people who have decades ahead of them. The longer the time horizon, the more dramatic the impact: assets contributed early have years to grow and compound, and every dollar of that growth can eventually be withdrawn completely tax-free. Here's why starting early matters:

Time is your biggest asset. Money contributed in your 20s or 30s has decades to compound completely tax-free. A $7,500 contribution at age 25 growing at 7% is worth over $113,000 by age 65 - all of it tax-free.

Lower tax bracket now. Young earners typically pay taxes at lower rates early in their careers. Paying tax on contributions today - before income grows - is often far cheaper than paying taxes on a much larger balance in retirement.

No RMDs, ever. Unlike a traditional IRA or 401(k), a Roth IRA never forces you to take distributions. Your money can keep growing tax-free for your entire lifetime if you don't need it.

Flexibility before retirement. Contributions (not earnings) can be withdrawn at any time without tax or penalty - making the Roth a useful emergency backstop while still building long-term wealth.

Tax-free inheritance. A Roth passed to heirs is one of the most efficient wealth transfer tools available. Beneficiaries generally have 10 years to withdraw the funds - all tax-free.

The bottom line: Young people are in the best position to benefit from a Roth - low tax rates today, maximum time for tax-free growth, and no obligation to ever touch the money. Starting early, even with small amounts, can make an extraordinary difference by retirement.

How Do I Build Assets in a Roth IRA?

There are three main ways to accumulate assets in a Roth IRA:

Direct contributions: Open a Roth IRA and contribute annually, subject to the contribution and MAGI

limits outlined above.

Backdoor Roth: If your income exceeds the MAGI limits, contribute to a traditional IRA and then convert

those assets to a Roth (see below).

Roth conversion: Roll over existing traditional IRA or 401(k) assets into a Roth IRA, paying income tax on

the converted amount in that year.

What Is a Backdoor Roth?

If your MAGI exceeds the direct contribution limits, you can still build Roth assets through a backdoor Roth strategy. The process is straightforward: make a non-deductible contribution to a traditional IRA (anyone can do this regardless of income), then immediately convert those assets to a Roth IRA. Because the contribution was made with after-tax dollars, only any growth between the contribution and conversion is taxable — making it most effective when done promptly after contributing.

Who Can Contribute to a Roth IRA? (2026 Income Limits)

Not everyone can contribute directly to a Roth IRA — eligibility is based on your Modified Adjusted Gross Income (MAGI). For 2026, the limits are:

Single / Head of Household: full contribution allowed below $153,000; no direct contribution allowed above $168,000.

Married Filing Jointly: full contribution allowed below $242,000; no direct contribution allowed above $252,000.

Married Filing Separately: contributions phase out almost immediately, with no contribution allowed above $10,000.

Important: Even if your income exceeds these limits, you can still build Roth assets through a conversion - there are no income limits on Roth conversions. High earners often use a "backdoor Roth" strategy: making a non-deductible traditional IRA contribution and then converting it to a Roth.

How Does It Differ from a Traditional IRA or 401(k)?

With a traditional IRA or 401(k), contributions are made pre-tax — reducing your taxable income today. The assets grow tax-deferred, but all withdrawals are added to your taxable income in the year they are taken. The IRS also requires minimum distributions beginning at age 73. A Roth flips this equation: you pay taxes now, and withdrawals later are tax-free with no RMD requirement.

What Is a Roth Conversion?

A Roth conversion moves assets from a traditional IRA or 401(k) into a Roth IRA. The converted amount is treated as taxable income in the year of the conversion. Conversions can be done all at once or gradually over several years - often called a “ladder” strategy.

Key Things to Know Before Converting

Tax impact: The converted amount is added to your taxable income for that year and may push you into a higher bracket.

Secondary effects: Higher income from a conversion can affect Medicare IRMAA surcharges, Social Security taxation, and ACA premium subsidies.

Pay taxes from outside: Pay the tax bill from outside funds — not from the IRA itself — to preserve the full value of the Roth.

5-year rule: Each conversion has its own 5-year clock for penalty-free withdrawal of converted principal if you are under age 59½.

When Does a Conversion Make the Most Sense?

Low-income years — job transition, sabbatical, or early retirement gap before Social Security begins.

Years with large deductions that can offset the conversion income.

Before age 73, to reduce future RMD obligations and the taxes that come with them.

During market downturns, when account values are lower — less taxable income, same future growth potential.

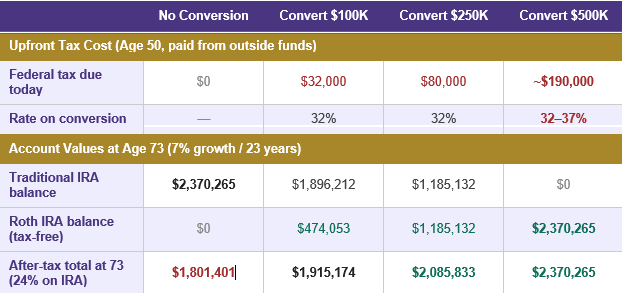

Convert or Not? See the Numbers

The table below compares account balances at age 73 across four conversion amounts, assuming a $500,000 IRA at age 50, 7% annual growth, and a 24% retirement tax bracket.

Questions to Ask Before Converting

Will my tax rate be higher or lower in retirement than it is today?

Do I have at least 10 years for tax-free growth to outweigh the upfront cost?

Can I pay the tax bill from outside funds without touching the IRA?

Should I convert all at once or use a multi-year ladder strategy?

Have I modeled the impact on Medicare, Social Security, and any subsidies?

Bottom line: There is no one-size-fits-all answer — every financial situation is different. That said, a ladder approach — converting a portion of your IRA each year over several years — is generally the most tax-efficient strategy for most people.

Please contact us at (973) 635-4275 to discuss Roth conversions or any other financial planning and wealth management topics.

Brian McGeough

Senior Relationship Manager

Disclosure

Chatham Wealth Management is registered as an investment adviser with the SEC. SEC registration does not constitute an endorsement of the firm by the Commission, nor does it indicate that the adviser has attained a particular level of skill or ability.

Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be profitable for a client's portfolio.